SIP Calculator: Your Guide to Smart Systematic Investing

A SIP Calculator is an essential financial tool that helps you visualize how small, regular investments can grow into substantial wealth over time. Whether you're planning for retirement, a child's education, or a dream home, understanding the power of systematic investing is the first step toward achieving your financial goals.

This calculator eliminates guesswork from financial planning by showing you exactly how much your monthly investments could be worth in the future, based on your chosen amount, time horizon, and expected returns. It's part of our comprehensive suite of Savings Retirement Calculators designed to help you build wealth methodically.

Why every investor needs a SIP calculator:

- Goal Planning: Set realistic financial targets for major life events

- Discipline Tracking: See the impact of consistent investing habits

- Return Projection: Understand potential growth with different return scenarios

- Risk Assessment: Evaluate how market fluctuations might affect your investments

- Comparative Analysis: Compare SIP with other investment strategies

By combining this tool with our EMI Calculator, you can balance your investments with liabilities for complete financial health.

Real-Life SIP Success Stories

Rahul's Education Fund: From ₹5,000 to ₹25 Lakhs

Rahul started a SIP of ₹5,000 per month when his daughter was born, aiming to build an education fund for her college. With an expected return of 12% annually, he wanted to know how much he'd have when she turned 18.

Investment Analysis:

- Monthly Investment: ₹5,000

- Investment Period: 18 years

- Expected Annual Return: 12%

- Total Amount Invested: ₹5,000 × 12 × 18 = ₹10,80,000

- Estimated Future Value: ₹25,67,842

- Wealth Gained: ₹14,87,842 (138% growth)

- Monthly equivalent: ₹11,892 per month growth through compounding

- Key insight: 62% of the final amount came from investment returns, not principal

Rahul's story demonstrates how consistency and time can transform modest monthly contributions into life-changing amounts. For retirement planning, consider using our Retirement Savings Calculator.

Priya's Retirement Planning: Starting Late but Catching Up

Priya began investing at age 35, worried she was too late for retirement planning. She started a SIP of ₹15,000 monthly, planning to invest until age 60.

Retirement Planning Analysis:

- Monthly Investment: ₹15,000

- Investment Period: 25 years (age 35 to 60)

- Expected Annual Return: 10%

- Total Amount Invested: ₹15,000 × 12 × 25 = ₹45,00,000

- Estimated Future Value: ₹1,79,89,678

- Wealth Gained: ₹1,34,89,678 (300% growth)

- Monthly income potential: ₹1,20,000 per month at 8% withdrawal rate

- Lesson: It's never too late to start, but starting earlier always helps

Priya's case shows that even with a late start, disciplined investing can still build substantial retirement corpus. For understanding how interest compounds, use our Compound Interest Calculator.

Ankit's Home Down Payment: Short-Term Goal Achievement

Ankit wanted to save ₹20 lakh for a home down payment in 5 years. He needed to calculate how much to invest monthly through SIP to reach his target.

Goal-Based Calculation:

- Target Amount: ₹20,00,000

- Time Horizon: 5 years

- Expected Annual Return: 11%

- Required Monthly SIP: ₹26,450

- Total Investment: ₹26,450 × 12 × 5 = ₹15,87,000

- Returns Generated: ₹4,13,000

- Alternative: Extend to 7 years reduces monthly requirement to ₹17,200

- Strategy: Balanced fund with moderate risk for short-term goal

Ankit learned that for shorter timeframes, he needed larger monthly contributions or had to extend his timeline. For home loan planning, check our Home Loan Calculator.

Understanding SIP: The Systematic Investment Plan

What Exactly is SIP?

A Systematic Investment Plan (SIP) is a disciplined approach to investing where you invest a fixed amount regularly (monthly, quarterly, etc.) in mutual funds. Unlike lump-sum investments where you invest a large amount once, SIP spreads your investment over time, making it more manageable and less intimidating.

Key Features:

- Regular Investments: Fixed amounts invested at regular intervals

- Flexibility: Start, stop, increase, or decrease investments anytime

- Accessibility: Can start with as little as ₹500 per month

- Automation: Automatic deductions from your bank account

- Market Timing Elimination: No need to predict market movements

For comparing investment options, use our ROI Calculator.

The Mathematical Formula Behind SIP Calculations

SIP Future Value Formula:

FV = P × [{(1 + r)ⁿ - 1} / r] × (1 + r)

Where:

FV = Future Value of SIP investments

P = Monthly investment amount

r = Monthly rate of return (annual rate ÷ 12)

n = Total number of months (years × 12)

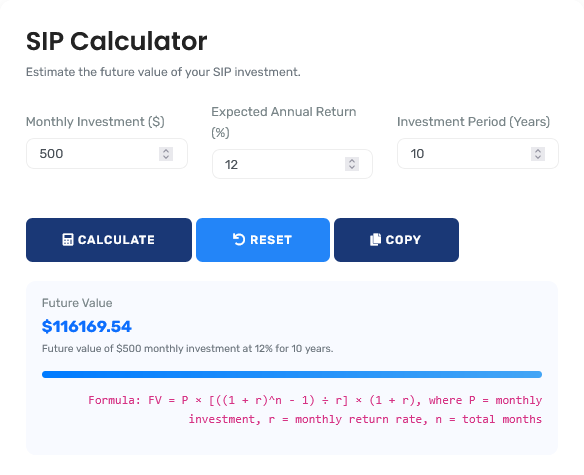

Example Calculation:

₹5,000 monthly for 10 years at 12% annual return:

P = 5000, r = 12%/12 = 1% = 0.01, n = 10×12 = 120 months

FV = 5000 × [{(1.01)^120 - 1} / 0.01] × 1.01 = ₹11,61,695

Key Insight: The (1 + r) at the end accounts for investments made at the beginning of each period.

SIP vs. Lumpsum: Which is Better?

| Aspect | SIP (Systematic Investment) | Lumpsum (One-time Investment) | Best For |

|---|---|---|---|

| Market Timing Risk | Low - investments spread over time | High - entire amount invested at once | SIP for risk-averse investors |

| Discipline | High - regular investing habit | Low - depends on investor discipline | SIP for consistent wealth building |

| Initial Capital Requirement | Low - start with small amounts | High - requires large upfront capital | SIP for beginners and salaried individuals |

| Rupee Cost Averaging | Yes - buys more units when prices low | No - buys at current market price only | SIP for volatile markets |

| Potential Returns | Moderate but consistent | Higher if timed correctly | Lumpsum in bull markets, SIP in uncertain markets |

Power of Compounding in SIP Investments

| Monthly SIP | 10 Years | 15 Years | 20 Years | 25 Years | 30 Years |

|---|---|---|---|---|---|

| ₹5,000 | ₹11.6 lakhs | ₹23.2 lakhs | ₹42.3 lakhs | ₹73.5 lakhs | ₹1.25 crores |

| ₹10,000 | ₹23.2 lakhs | ₹46.4 lakhs | ₹84.6 lakhs | ₹1.47 crores | ₹2.50 crores |

| ₹20,000 | ₹46.4 lakhs | ₹92.8 lakhs | ₹1.69 crores | ₹2.94 crores | ₹5.00 crores |

| ₹50,000 | ₹1.16 crores | ₹2.32 crores | ₹4.23 crores | ₹7.35 crores | ₹12.5 crores |

Step-by-Step Guide to Using SIP Calculator

5 Simple Steps to Plan Your SIP:

- Define Your Goal: What are you saving for? (Retirement, education, home, etc.)

- Set Time Horizon: How many years until you need the money?

- Determine Target Amount: How much will you need?

- Calculate Monthly SIP: Use calculator to find required monthly investment

- Review and Adjust: Can you afford it? Adjust amount or timeline if needed

This systematic approach ensures your investments align with your financial goals and capacity. For comprehensive financial planning, explore our full range of Finance Calculators.

Common SIP Investment Mistakes to Avoid

The "Stop During Market Dips" Mistake

Common Error: Stopping SIP when markets fall.

Why It's Wrong: Market dips are when SIP works best - you buy

more units at lower prices.

Data: Continuing SIP through the 2008 crisis yielded 18% annual

returns by 2013.

Solution: Treat SIP as non-negotiable monthly commitment, like

rent or EMI.

Chasing Past Performance

Many investors choose funds based solely on last year's top performers, which often underperform next year.

Smart Approach:

• Look at 5-10 year consistent performance, not 1-year star performers

• Consider fund manager tenure and strategy consistency

• Diversify across 3-4 quality funds rather than betting on one

• Review performance annually, but avoid frequent switching

Remember: Past performance doesn't guarantee future returns. Focus on fund fundamentals and your risk tolerance.

For business investment calculations, try our Profit Margin Calculator.

Tax Benefits of SIP Investments

ELSS Funds: Tax Saving with Growth Potential

Scenario: ₹1.5 lakh annual investment in ELSS through SIP for tax saving under Section 80C.

-

Tax Benefit Calculation:

- Maximum deduction: ₹1.5 lakh under Section 80C

- Tax saved (30% bracket): ₹1,50,000 × 30% = ₹45,000 annually

- Effective investment cost: ₹1,05,000 (₹1,50,000 - ₹45,000 tax saved)

-

Growth Projection:

- Annual investment: ₹1.5 lakh (₹12,500 monthly)

- Investment period: 15 years

- Expected return: 12% annually

- Future value: ₹62.3 lakhs

- Wealth created: ₹39.8 lakhs (excluding tax benefits)

-

Lock-in Consideration:

- 3-year lock-in per installment

- Encourages long-term investing discipline

- First installment available after 3 years, then staggered availability

For income tax calculations, use our Income Tax Calculator.

SIP Strategy Based on Investment Horizon

| Time Horizon | Recommended Fund Type | Risk Level | Expected Return | Suggested SIP Amount | Exit Strategy |

|---|---|---|---|---|---|

| Short-Term (1-3 years) | Debt Funds, Liquid Funds | Low to Moderate | 6-8% annually | Based on goal amount | Switch to safer options 6 months before need |

| Medium-Term (3-7 years) | Balanced/Hybrid Funds | Moderate | 9-11% annually | Increase by 10% yearly | Start shifting to debt 1-2 years before goal |

| Long-Term (7+ years) | Equity Funds, Index Funds | Moderate to High | 11-14% annually | Start with what's comfortable, increase with salary | Review annually, rebalance as needed |

| Very Long-Term (15+ years) | Aggressive Equity, Small Cap Funds | High | 12-15% annually | Be consistent, don't stop during downturns | Systematic withdrawal in retirement |

When to Increase Your SIP Amount

Smart Times to Step Up Your SIP:

- Annual Salary Increase: Allocate 50% of increment to SIP increase

- Bonus/Incentive: Consider one-time additional investment

- Reduced Expenses: EMI completion, child education completion

- Windfall Gains: Inheritance, property sale proceeds (partial allocation)

- Market Corrections: Temporary increase during market dips

Step-up SIP Strategy: Increase SIP by 10% annually can reduce required investment period by 30-40% for same goal.

For calculating how inflation affects your goals, use our Inflation Calculator.

Practical SIP Planning Examples

Example 1: Child's Higher Education (15-Year Plan)

Goal: ₹50 lakhs for child's foreign education in 15 years

Solution:

Required Monthly SIP at 12% return: ₹12,350

Total Investment: ₹12,350 × 12 × 15 = ₹22,23,000

Returns Generated: ₹27,77,000 (125% of investment)

Alternative: Start with ₹10,000, increase by 10% annually =

Achieves same goal

Example 2: Retirement Planning (30-Year Journey)

Goal: ₹5 crores retirement corpus in 30 years

Solution:

Required Monthly SIP at 11% return: ₹20,150

Total Investment: ₹20,150 × 12 × 30 = ₹72,54,000

Returns Generated: ₹4,27,46,000 (589% of investment)

Strategy: Start with ₹15,000 at age 30, increase by ₹1,000

annually

For retirement planning, use our 401k Calculator for US-style retirement accounts.

Key Insight: SIP success depends more on time in the market than timing the market. Starting early, staying consistent, and allowing compounding to work are more important than chasing the highest returns. Even modest monthly investments can create substantial wealth with sufficient time. Remember to review your SIP portfolio annually and rebalance as needed. For comparing different financial products, check our APR Calculator.

Quick SIP Reference Guide

Starting Your SIP:

- Choose a mutual fund based on your goal horizon and risk tolerance

- Complete KYC if not already done

- Fill SIP registration form with bank mandate

- Select date (1st-10th recommended for salary crediting alignment)

- Start with comfortable amount, increase gradually

Monitoring Your SIP:

- Check quarterly statements, not daily NAV

- Review performance annually against benchmark

- Rebalance if fund consistently underperforms category average

- Don't stop during market downturns - this is when SIP works best

- Consider tax implications before redeeming

Remember: SIP is a marathon, not a sprint. Patience and consistency beat market timing.

Frequently Asked Questions

Most mutual funds allow you to start a SIP with as little as ₹500 per month. Some funds may have slightly higher minimums, but generally, SIPs are designed to be accessible to investors with limited capital. The key is to start with what you can afford consistently, then increase gradually as your income grows.

Yes, SIP investments in open-ended mutual funds (except ELSS) can be redeemed anytime. However, it's recommended to stay invested for at least 3-5 years to ride out market volatility and benefit from compounding. ELSS funds have a 3-year lock-in period from each investment date. Early withdrawals may also have tax implications depending on your holding period.

Most fund houses allow 1-2 missed payments without penalty. After consecutive missed payments (usually 3), your SIP may be canceled automatically. Missing payments disrupts your investment discipline and compounding benefits. If you anticipate cash flow issues, consider reducing the SIP amount temporarily rather than stopping completely.

Consider these factors: 1) Investment horizon (short/long-term), 2) Risk tolerance, 3) Financial goals, 4) Fund performance history (5+ years), 5) Expense ratio, 6) Fund manager experience. Diversify across 2-4 funds rather than putting all money in one. Start with large-cap or balanced funds if you're new to investing.

No, SIP returns are market-linked and not guaranteed. Returns depend on fund performance, which in turn depends on market conditions. However, SIP reduces risk through rupee cost averaging and eliminates the need for market timing. Historically, SIPs in equity funds have delivered 10-15% returns over 10+ year periods, but past performance doesn't guarantee future results.

Yes, absolutely! Continuing SIP during market downturns is when rupee cost averaging works best. You purchase more units at lower prices, which boosts long-term returns when markets recover. Historical data shows investors who continued SIP through the 2008 financial crisis saw their portfolios recover and grow significantly within a few years.